Table of Content

Whatever your budget and home wish-list preferences, HomeFinder will make your search stress-free with our easy-to-navigate portal and search functions. Filter your search to find the perfect possibilities from the thousands of listings on our site. Scroll through the listings to see photos or virtual tours, information about the year built, the home’s amenities, and more. A credit counselor may also suggest a Credit Card Forgiveness program, offered by a select few nonprofits.

Yet although it tends to be easier to enter into a rent-to-own agreement, there are still requirements you may need to meet before a program may be willing to work with you. As a buyer, the idea behind rent-to-own is to give you time to work on obstacles that are preventing you from qualifying for a mortgage. Credit problems, debt-to-income ratios that are too high, and other challenges may all fall into this category. Hiring a qualified real estate attorney to explain the contract can help you understand your rights and obligations in a rent-to-own agreement.

How to Find Rent-to-Own Homes & Secure Your Dream Property

Most contracts allow the landlord to keep the rent credit money, even in an option agreement, if the renter decides not to buy. Some contracts have either a premium payment or a monthly credit. Be sure you understand yours before you sign it, and be prepared to walk way, if it doesn’t work for you. Depending on the terms of the contract, you may be responsible for maintaining the property and paying for repairs. Usually, this is the landlord's responsibility, so read the fine print of your contract carefully.

To have the option to buy without the obligation to buy, it needs to be a lease-option contract. Rent-to-own leases work best when you know exactly where you want to live. Both choices are similar since they both allow you to lease a home for 1 – 3 years and then buy it at the end of the term. However, there are some contractual differences between the two that you should know. Lesly Gregory has over 15 years of marketing experience, ranging from community management to blogging to creating marketing collateral for a variety of industries. She currently lives in Atlanta with her husband, two young children, three cats and assorted fish.

Rent-to-Own vs. Mortgage: The Differences and Advantages

Chris and the Dream team have been great to work with in getting me into the right house for my family. We are renting now and look forward to buying as soon as we qualify for our VA mortgage. Please note, if you pay your rent late two or more times during the initial lease , the renewal option is void. A minimum of $5,000 from savings, 401k plan or gift from a family member is required in order to be considered for the Dream America Program ($8,000 if your FICO is below 550).

This makes us more attractive to sellers and generally allows us to get a better deal. To state the obvious, rent is more expensive than your cost of ownership once you obtain a mortgage! That is why we offer a penalty-free early lease termination when you buy your Dream home.

How to Fill Out a Schedule E Form as a Landlord

He notes that when a home under-appraises, it isn’t always bad, at least for the would-be buyer. It gives you the chance to renegotiate the contract and can save you money if the seller agrees to lower the purchase price. Owning a home is the best way for many people to build solid financial footing, not only for themselves, but for their children.

If they have a high credit score, a landlord may get the reassurances they need from your combined number than with yours alone. Consider doubling the security deposit so that your landlord has a buffer if rent is late. You'll get this money back once you move out, assuming you leave the home in good condition. If you have any negative marks on your credit report, try to get them removed.

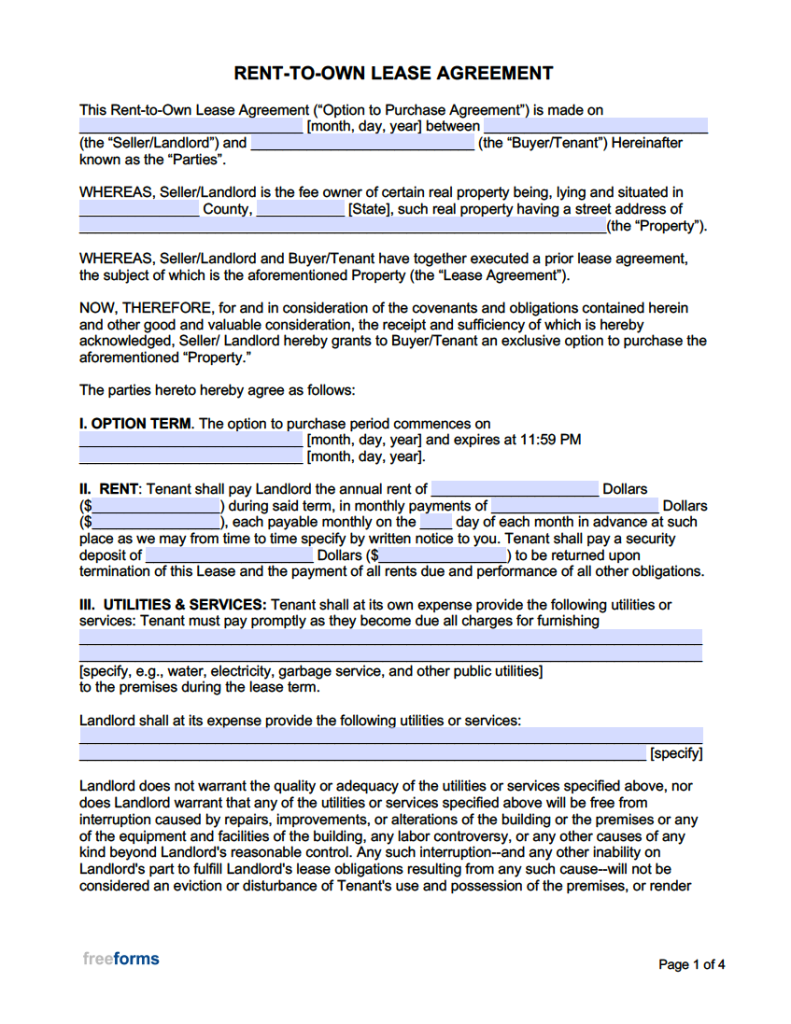

Research the Contract

Her work has appeared in Business Insider, Good Housekeeping, TODAY, E! Divvy, for example, accepts applicants with a FICO® Scores as low as 550. Coldwell Banker, by comparison, requires a minimum household credit score of 600 or above. Earnest money is a deposit made to a seller, often in real estate transactions, that shows the buyer's good faith in a transaction.

Rent-to-own gives the renter time to improve bad credit while locking in a home to buy. This only works if your credit improves enough to get a mortgage by the end of the agreement’s term. The median sale price for a single-family home at the beginning of 2022 was $353,900, which means a 20% down payment of $78,780, which is a heavy financial lift for most consumers. Lower-income buyers have the option of an FHA loan, with a 3.5% down payment of $12,386, but that’s still a stretch for many budgets. As described above, your Purchase Price is set when your lease begins.

With this program, the minimum credit score is 500, with a 50% maximum DTI. Home Partners property management company, Pathlight Property Management, prepares it for tenants to move in. Residents have the option to purchase the home at any time during the lease. If you do not renew the lease and don’t choose to buy the home, you can then move out without penalty. Through the Home Partners program, prospective rent-to-own homebuyers start by filling out a pre-qualification application.

You’ll give up your claim to the home and all your rent credit you’ve accumulated if you cannot get funding for your home by the end of the lease. The homeowner can also sue you for breach of contract if you don’t buy the home. A lease-purchase agreement works in almost the same way as a lease-option agreement. You still lease the home for a few years and put a certain percentage of your rent toward a down payment to buy the home. You can walk away from the option and allow it to expire if you choose not to buy the property.

You can also use a credit monitoring service to keep track of your credit score and credit report. Each of these elements can flush out a credit score, explaining why it's where it is on the scale, but also providing insight into any major red flags for you as a renter. The reason there are three different major credit bureaus is that each one can generate a slightly different report. Credit scores can differ as a result, so the person checking your credit may want an average score. Last, hire an attorney or work with a top real estate agent so that you have a professional who can look over the contract and watch out for your best interests.

In either of these scenarios, a collection account could show up on your credit report. Some would-be homeowners have horror stories of surprise foreclosures during rent-to-own agreements, unpaid property taxes, and more. The Federal Trade Commission warns of outright scams you could face as well. In other words, you can test out a home and the neighborhood it’s located in before you make a long term commitment. If you rent a home with the option to buy and discover that it’s not the right place for your family, you can back out and opt not to move forward with the purchase.

However, doing so will forfeit both your option fee and your rent credits. If no other strategy works when it comes to your credit score, there are no-credit-check landlords out there. While they're harder to find and may have higher rent prices, going this route saves you from dealing with your credit score at all. Credit reports aren't always expressive of your current financial situation. A mistake in the past could follow you around for quite a while, so to establish why now is different, you may have to produce evidence outside your credit score.